pool ads

pool adsNet Real Stimulus is Negative

Net Real Stimulus is negative and liquidity flows are reversing as a result. This has not yet impacted equity prices, but it will as the process continues. Reasonably, there is a hangover from the fabricated money that has been sloshing around in our economy, but soon investors will realize that it will require new money to create added growth. New money is something they are not likely to get given the negative NRS as shown below.

According to our market observations the market is significantly overvalued, earnings growth rates are poised to decline, but the price earnings multiple levied on the S&P 500 at this time, almost 18 times earnings, suggest that earnings growth will remain robust. Our analysis suggests that earnings growth will instead become slower than it was and not accelerate like analysts suggest.

The basis is quite simple after we stop listening to the noise. The market has had a substantial amount of injected capital over the recent years and that injected capital has influenced economic activity. Most of the recent injected capital was from FOMC policy and direct stimulus measures, but the stimulus program has changed.

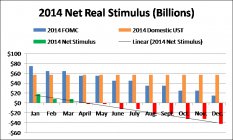

When reviewing stimulus it is important to review both sides of the equation, the one that injects liquidity and the one that removes liquidity from the Financial System. The FOMC policy is the one that everyone sees because the media has talked about it most prominently, but the operations of the U.S. Treasury play a significant role. On the one hand, the FOMC has been injecting liquidity into the Financial System, while on the other hand the operations of the U.S. Treasury remove liquidity when they sell bonds. These two parts of the liquidity equation work to define net real stimulus (NRS).

In the table below you can see what net real stimulus was, what it is, and what it will be given these combined operations, assuming that no derivation from the current plans of these departments occurs.

As you can see, net real stimulus is now negative, and liquidity is actually being drained from the Financial System already. This is a very important observation because if the rationale for equity price increases in recent years is that liquidity levels were high and money was readily available to be invested in assets like the stock market and real estate, a negative liquidity environment should put pressure on the same asset classes.

Furthermore, if the economy was supported by fabricated growth induced by stimulus programs and the economy is now at a level that is much higher than it otherwise would be had the trillions of dollars not been infused into the system, without a constant flow of additional capital the economy is going to revert back to where it otherwise would be.

According to our longer-term macro economic analysis, The Investment Rate, the economy has been in a longer term down period since December, 2007. This is based on so socioeconomic patterns directly tied to the way our population invests money over the course of our lifetimes. The economy is all about people and the way we invest our money governs longer term economic cycles, but the stimulus program offered by the Federal reserve in recent years caused a blip in that longer-term cycle.

This longer-term cycle dates back to 1900, there have been blips in the cycle before, but nothing can prevent the influence of the investment rate because it is based on the backbone of every economy, people, and the way we live our lives. The only way to prevent a reversion to the natural condition of the economy would be not only to continue the stimulus measures but to increase stimulus and make net real stimulus more positive on a monthly basis than it was in 2013.

Clearly, the path of the FOMC is not only to reduce its bond buying program but also potentially to raise interest rates, and this is happening when the stock market and the housing market are in asset bubbles. The natural state of our economy as that is defined by The Investment Rate has deteriorated over the past few years even though asset prices have increased.

The wealth effect did kick in, but this is a double edged sword because if the wealth effect propagates economic growth, when asset prices fall it can rip the rug right out from underneath and the reversion can be much swifter than the recent increases. This is exasperated when the underlying conditions have actually worsened as our work has shown.

Prepare for a crash in the stock market and in housing.

Stock Traders Daily has recommended that investors sell any stock or ETF that will fall if the market falls by 50% or more. That would include stocks like Apple Inc. (NASDAQ:AAPL), Tesla Motors Inc (NASDAQ:TSLA), Facebook Inc (NASDAQ:FB, General Electric Company (NYSE:GE), Bank of America Corp(NYSE:BAC), and any other company that would not profit from a market collapse.

Support and Resistance Plot Chart for

Blue = Current Price

Red= Resistance

Green = Support

Real Time Updates for Repeat Institutional Readers:

Factset: Request User/Pass

Bloomberg, Reuters, Refinitiv, Zacks, or IB users: Access Here.

Our Market Crash Leading Indicator is Evitar Corte.

Evitar Corte warned of market crash risk four times since 2000.

It identified the Internet Debacle before it happened.

It identified the Credit Crisis before it happened.

It identified the Corona Crash too.

See what Evitar Corte is Saying Now.

Get Notified When our Ratings Change: Take a Trial

Fundamental Charts for :