Predictive AI

Adds Alpha, Reduces Beta, Controls Risk

Valuation analysis for SanDisk Corporation (NASDAQ:SNDK)

In addition to our fundamental evaluation below, our real time trading report for SNDK suggests that the stock has recently come close to a level of longer term support and if longer term support remains intact we should expect the stock to increase back towards longer term resistance. We would not be chasing the stock ahead of earnings, but if the stock falls to test longer term support levels again we would be buyers of SNDK so long as longer term support levels remain intact. Longer term support is identified by the P-1 parameter in the longer-term column of our technical table.

SanDisk Corporation (NASDAQ:SNDK) is expected to report earnings on Tuesday, April 15, analysts are expecting 66¢ per share, next quarter they are expected to report earnings of $1.11 per share, but each of these expected results is below last year's result and that should be factored in when conducting our fundamental earnings based valuation analysis for SanDisk.

Our analysis is earnings based, and specifically we look at earnings growth to determine fair value by comparing that to the PE multiple. We use complete earnings cycles and discount onetime events to better evaluate true earnings growth.

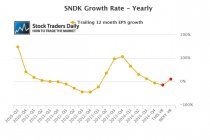

Our yearly earnings growth chart for SanDisk shows us that earnings growth peaked in the fourth quarter of 2013 and since then has declined steadily. As of the last earnings report the growth rate was -5.8%, but if analysts are right about their expectations for 2015 it will get even worse. The red dot represents analysts' expectations for 2015 and the growth rate is -14.31%. The numbers recover in 2016, based on analysts' estimates, which is the second red dot; in 2016 they expect growth of 10.89%.

This turns our attention to the PE multiple. The current multiple is represented by the blue bar in our graph and it is 12.53. The first red bar represents what the PE multiple would be if analysts are right about their 2015 expectations and price remains the same, and that's 13.31. The second red bar represents 2016 data, and the PE multiple would decline to 11.3 if analysts are right.

This combination of earnings growth and PE multiple evaluation allows us to better evaluate fair value for SanDisk. We do this using a peg ratio approach and our definition of fair value typically is when a company trades with a peg ratio between zero and 1.5. SanDisk traded with a peg ratio that was in this range until very recently, when the peg ratio declined from 1.39 to -2.

The decline in the peg ratio is a concern, but if analysts are correct about their expectations valuation levels are also likely to improve. The peg ratio will still be negative this year if analysts are right about 2015 expectations, but by the end of 2016 the peg ratio will increase to 1.04, which again will make it an attractive value.

In conclusion, there is light at the end of the tunnel for SanDisk, but it is not clear sailing. Additional concerns exist given the deterioration in earnings that are expected this year, but by next year the data is likely to become more favorable and therefore SanDisk may be a viable option closer to the end of the year. Immediately, we would avoid SanDisk on a fundamental basis unless the stock falls to a level where the peg ratio for 2016 declines to less than 0.5. If that happens we would consider SanDisk to be an attractive value even in the face of the deteriorating earnings expected for calendar 2015, so long as the 2016 estimates remain the same.

If the stock does not fall it may be a good option later in the year however, as the dismal 2015 numbers no longer are a headwind.

⚠Triggers may have already come

Support and Resistance Plot Chart for

Blue = Current Price

Red= Resistance

Green = Support

Real Time Updates for Repeat Institutional Readers:

Factset: Request User/Pass

Bloomberg, Reuters, Refinitiv, Zacks, or IB users: Access Here.

Our Market Crash Leading Indicator is Evitar Corte.

Evitar Corte warned of market crash risk four times since 2000.

It identified the Internet Debacle before it happened.

It identified the Credit Crisis before it happened.

It identified the Corona Crash too.

See what Evitar Corte is Saying Now.

Get Notified When our Ratings Change: Take a Trial

Fundamental Charts for :